In the last post, we talked about the purpose of FI. You may have looked at the list of potential “whys of FI” and asked how that is different than normal retirement. Busted. It isn’t.

Remember just after I asked about what your goals are, I asked how fast do you want to get there? That’s the next big thing you need to decide.

I don’t care how old you are or what your time horizon is. You’re allowed to have the same goals. Maybe you’re just planning for it earlier or later than the next person. Traditional FI (aka regular retirement) is for those planning to be FI in their 60’s (maybe even 50’s). I would suggest that early FI would be for those targeting sometime in their 30’s or 40’s. This is what is referred to as FIRE (Financial Independence, Retire Early).

The key difference between traditional and early FI are societal norms. Society expects you to work until you’re in your 60’s (maybe 50’s if you’ve been prudent with saving or have an early pension option with your employer). Remember the commercials about “Freedom 55?” How many people laugh [hopelessly] when reminiscing about those ads? That’s because most people don’t retire that early.

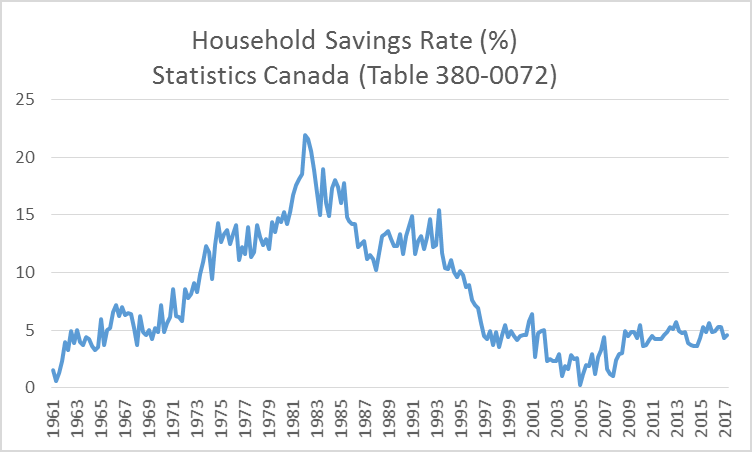

What drives the expectation of retiring in your 60’s? There are lots of reasons, but it comes down to your savings rate (what percent of your income do you save). The average Canadian household savings rate has been hovering around 5% for the last 20 years (See chart below). The 20 years before that was around 10-15%. Even in the 10-15% savings range, you are likely going to need 30-40 years to save enough for FI. Nothing wrong with that, you’re still better than average! However, most people I know do not like the idea of working full-time for 30 to 40 years and then benefiting from seniors’ discounts and driving your convertible to the lawn bowling tournament. This is not most people’s definition of happiness (but there’s nothing wrong if it is).

To target FI in your 30’s and 40’s will require a savings rate more like 40-60% (assuming you’re still in your 20’s or early 30’s). The math of this is relatively straightforward, but a topic for another day. Just trust me for now. The point is, if you want to get to FI earlier, you have to save more money. Ay Ay Captain Obvious!

Admittedly, this will be easier for those with high incomes, but there are also lots of examples of people on modest incomes achieving this.

If you’re saving around 50% of your income, you probably aren’t exhibiting all the regular behaviours of your peers. You didn’t lease a new car, you didn’t get the largest house the bank would let you, you don’t send your kids to private school (or an out-of-town university), you don’t go travelling around the world in fancy hotels, and so on. Most people would do all those things if they had the money. Early FI-ers have the money, but choose to save it rather than spend it on the same things as their peers.

The early FI group has the same goals as the traditional FI group, but they save a lot more of their income in order to get there faster.

The speed to which you want to reach FI is as important as the goal itself, as this will greatly affect how much you need to save each year. The more aggressive your goal, the more aggressive your savings plan has to be.

Conclusion

If you have an idea of what would make you happy, now you have to go the next step and decide when you want that to be. Once we have an idea of what and when, then we can start talking about how much money is needed.