I wish we could avoid talking about taxes, but unfortunately, there are a lot of tax implications to financial planning decisions. Sometimes it can feel like splitting hairs (in which case I’ll try to gloss over it), but in later posts we’ll talk about significant tax planning things such as:

- When to contribute money to your RRSP

- Income splitting techniques (if you have a significant other and/or have kids)

- What type of investments to buy

- Figuring out how much money you’ll need in retirement

The first two almost entirely relate to tax planning, while it’s a smaller component of the latter two. These are all great things that we will talk about later. All I’m saying here is that it’s important to have a general understanding of how our personal income tax system works.

Income Tax Brackets

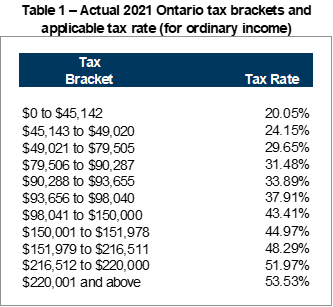

An income tax bracket is expressed as a range of income. Within that range, a certain tax rate is applied. The federal government and each provincial government have different tax brackets. Unfortunately, the brackets are not the same which means that there are many small brackets when you combine the federal tax with your provincial tax. For example, there are 11 tax brackets in Ontario for 2021 as follows:

For example, you can see above that income in the $49,021 to $79,505 range is taxed at 29.65%.

You can easily find this table on taxtips.ca for other provinces (and other years), but since most of the people I talk to about this are in Ontario, I’ll use that for my examples.

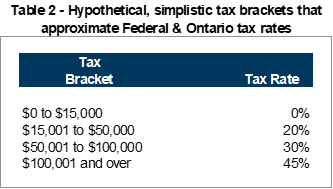

It is cumbersome to deal with 11 tax brackets, so for illustrative purposes, let’s distill this down to 4 brackets. We’ll then bring it back to real life later. I’ve strategically chosen the following 4 hypothetical tax brackets, because they will actually approximate the results of using all 11 tax brackets (as long as your income is less than $220,000):

How the Tax Rates are Applied

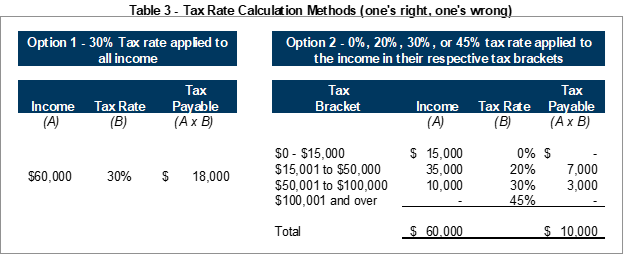

It is obvious that higher income ranges are taxed higher, but how are the rates applied? Let’s calculate those for someone earning $60,000 per year.

Looking at table 2 above, we know someone earning $60,000 is in the 30% tax bracket.

Here are two ways (one right, one wrong) to calculate the tax payable – note the $8,000 difference between the two calculations.

Have you made your bet on which one is the correct calculation? Option 1 is very simple and creates higher tax revenue, so it would be a good candidate for the CRA to choose.

Nope! Option 2 is the correct calculation even though the tax payable is $8,000 less!

Why the heck would the CRA choose a method that is more complicated and gets them less tax? The answer is they’re trying to be fair. I’m serious…the CRA tries to keep things fair, at least between similar tax payers. Consider whether the following scenario is fair:

You’re discussing with a colleague about him taking on an extra shift at work. This shift pays 3x their regular rate – or about $1,000 (it’s a long shift!). Your colleague says something along the lines of “no way I’m doing that, it’ll put me in a higher tax bracket and I’ll pay more in taxes!” He continues “I’m earning a $50,000 salary now in the 20% tax bracket, if I earn a dollar more, I’ll jump up to the 30% tax bracket and pay 10% more tax ($5,000 = $50,000 x 10% higher tax bracket) on everything. The government man, I tell you!”

Now, would it be a logical to structure the tax system with these “cliffs” where people are actually worse off if they earn more money? I hope you’ll agree that that approach wouldn’t make much sense.

Fortunately, the CRA (or “government man,” however you wish to colloquially refer to the tax collection division) agrees that this isn’t fair.

The CRA has designed the tax system to always encourage people to earn more money. The way they do this is that only the amount earned over $50,000 is taxed at 30%. The tax rate on anything less than $50,000 does not change…it says at 20%, regardless of how much income you earn!

If that colleague took the extra shift, his $50,000 salary will still be taxed at 20% and only the extra $1,000 pay (i.e. the amount over $50,000) will be taxed at 30%. So, he will still have $700 more in his pocket if he takes that shift ($1,000 pay less 30% tax on that). He still has to pay taxes on the extra money earned, but it’s still a pretty lucrative option for one [long] days’ work. I say he should do it!

Linking this back to Table 3, your colleague is thinking about option 1 (all income would be taxed at the higher rate). That’s the simple, tempting, but (fortunately for us) unfair and incorrect. Option 2 is how income tax is actually calculated.

Real Life Example

This is all great in theory, but doing this for all the 11 actual tax brackets is a pain in the arse. I agree – I just use an online calculator. For calculating taxes, I like to use this calculator from Ernst & Young. If you’re reading this some year later, substitute “2021” in the URL for the current year and you should get the current rates.

There are a bunch of columns of output, the important ones are:

- Tax Payable

- Marginal Tax Rate (this is the “tax bracket” corresponding to the income level from table 1 above, for Ontario)

Let’s take the calculator for a spin. Click on the link and first type in $60,000 into the “taxable income” box and press “calculate”. The result for Ontario is:

- $10,622 tax payable (note this is a lot closer to Option 2 above than Option 1 from Table 3)

- 29.65% marginal tax rate (can you see that rate in table 1 above?)

This shows that if you’re in the 29.65% tax bracket, not all your income is taxed at 29.65%…otherwise you’d be paying $17,790 in tax ($60,000 x 29.65%). That’s a difference of over $7,000 compared to the actual $10,622 in tax you owe…amazing!

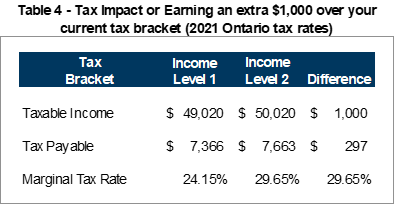

Another way to illustrate this is to compare incomes (using the EY tax calculator) that are just at and just above a tax bracket (similar to the extra shift conundrum your hypothetical colleague was discussing earlier):

This scenario is to highlight that earlier conversation with your colleague, but with real numbers. If you earn $1,000 over your current tax bracket, you pay, wait for it, only an extra $296.50 (it is not a coincidence that that equals the marginal tax rate for that higher bracket!).

What this means (for financial planning purposes) is that we can measure an incremental change to your taxes payable by only looking at your marginal tax rate (i.e. the rate for the tax bracket you’re currently in).

If you’re job hunting, taking an overtime shift, expecting a bonus, etc., use this calculator to see what the impact will be on your tax payable.

The Point

The main takeaway here is that earning more money can never result in less after tax income. The higher tax rate, if you “move up” a bracket, only applies to that extra income. All of your income below that bracket is taxed at the applicable lower rates.

Also, I’ve introduced the concept of a marginal tax rate (i.e. the current tax bracket you’re in) which is how we measure the tax impact from a change in your income. This is different (and more important) than your average tax rate, which we’ll dig into next.