When more than 50% of people rate themselves as above average, social psychologists call this illusory superiority.

You know how everyone, when self-assessing themselves, is smarter than average and better looking than average? Well, your marginal tax rate is higher than average….I guarantee it!

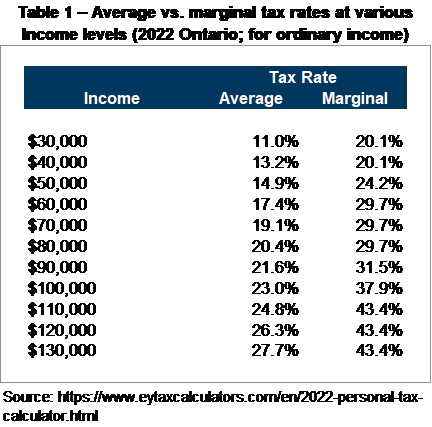

The following table shows the marginal tax rate and average tax rate at various income levels. As promised, the marginal tax rate is always higher than the average!

This is not a surprising result, mathematically, since Canada has a progressive tax system (which means income earned in higher tax brackets are taxed at higher rates).

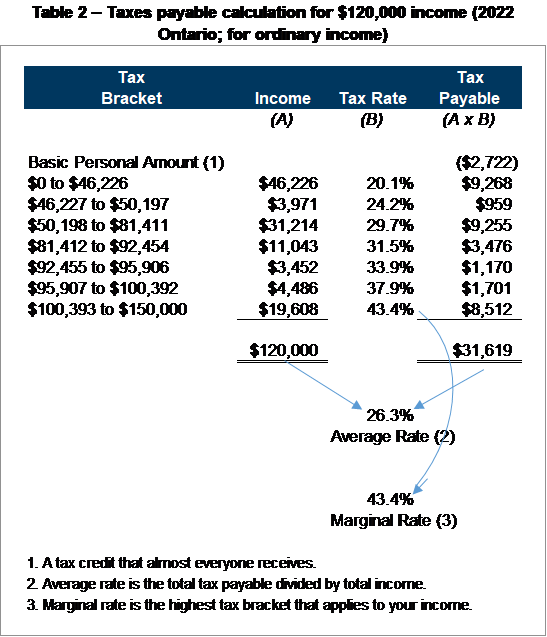

Does it surprise you that someone earning $120,000 only pays 26.3% of that in tax? However, if they earn an extra $1,000, that extra $1,000 will be taxed at 43.4%, or $434 of tax. Here’s how taxes are actually calculated for an income of $120,000:

I hope between the above table and our discussion in the last post, we can agree on what your average tax rate is versus your marginal tax rate. Very importantly, it is key to understand that your average tax rate is often far less than your marginal tax rate; it’s the marginal rate that most people focus on. And now you know that your marginal tax rate is always higher than your average tax rate.

Why is your marginal tax rate so important?

The marginal tax rate is important to measure changes in your taxable income (e.g. earn an extra $1,000 dollars which increases your taxable income or contribute $1,000 to your RRSP, which reduces your taxable income). In the example above at a $110,000 income level, if your taxable income goes up or down by $1,000, your taxes owed will go up or down by 43.4%, or $434.

Overall, your marginal rate is important for tax planning for situations such as:

How much tax you’ll pay if you earn an extra dollar

Rental income, side hustle, overtime (as discussed in the previous post)

How much tax you’ll be refunded if you contribute an extra dollar to your RRSP

How much tax you’ll save if you can income split with your spouse or kids

How much tax you can defer or avoid through other tax planning strategies

Why is your average tax rate important?

Average tax is important for estimating total taxes in your budget. If you’re planning to live on $56,000 after-tax when you retire, then you’ll need $69,000 before tax. That is because the average tax rate is about 19%, so $69,000 less $13,000 (rounded) in taxes equal $56,000.

To summarize, your average tax rate is important for:

Estimating after-tax income when budgeting for your annual expenses

Planning after-tax income needs in retirement

Now that you know the difference between marginal and average tax rates, I can assure you that you’re better than average! 🙂

More resources if you would like to read about this from different angles:

I wish we could avoid talking about taxes, but unfortunately, there are a lot of tax implications to financial planning decisions. Sometimes it can feel like splitting hairs (in which case I’ll try to gloss over it), but in later posts we’ll talk about significant tax planning things such as:

When to contribute money to your RRSP

Income splitting techniques (if you have a significant other and/or have kids)

What type of investments to buy

Figuring out how much money you’ll need in retirement

The first two almost entirely relate to tax planning, while it’s a smaller component of the latter two. These are all great things that we will talk about later. All I’m saying here is that it’s important to have a general understanding of how our personal income tax system works.

Income Tax Brackets

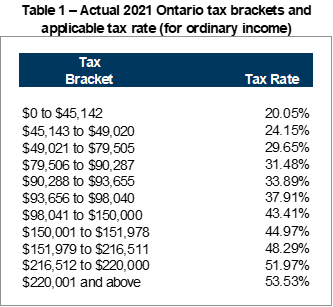

An income tax bracket is expressed as a range of income. Within that range, a certain tax rate is applied. The federal government and each provincial government have different tax brackets. Unfortunately, the brackets are not the same which means that there are many small brackets when you combine the federal tax with your provincial tax. For example, there are 11 tax brackets in Ontario for 2021 as follows:

For example, you can see above that income in the $49,021 to $79,505 range is taxed at 29.65%.

You can easily find this table on taxtips.ca for other provinces (and other years), but since most of the people I talk to about this are in Ontario, I’ll use that for my examples.

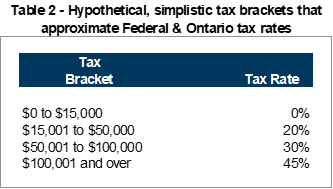

It is cumbersome to deal with 11 tax brackets, so for illustrative purposes, let’s distill this down to 4 brackets. We’ll then bring it back to real life later. I’ve strategically chosen the following 4 hypothetical tax brackets, because they will actually approximate the results of using all 11 tax brackets (as long as your income is less than $220,000):

How the Tax Rates are Applied

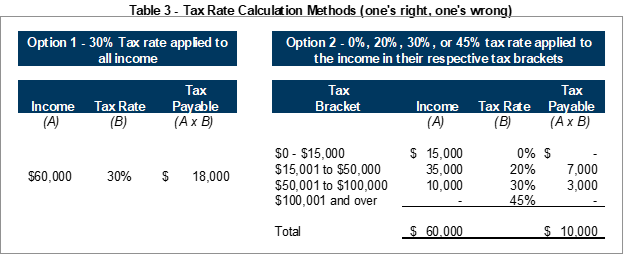

It is obvious that higher income ranges are taxed higher, but how are the rates applied? Let’s calculate those for someone earning $60,000 per year.

Looking at table 2 above, we know someone earning $60,000 is in the 30% tax bracket.

Here are two ways (one right, one wrong) to calculate the tax payable – note the $8,000 difference between the two calculations.

Have you made your bet on which one is the correct calculation? Option 1 is very simple and creates higher tax revenue, so it would be a good candidate for the CRA to choose.

Nope! Option 2 is the correct calculation even though the tax payable is $8,000 less!

Why the heck would the CRA choose a method that is more complicated and gets them less tax? The answer is they’re trying to be fair. I’m serious…the CRA tries to keep things fair, at least between similar tax payers. Consider whether the following scenario is fair:

You’re discussing with a colleague about him taking on an extra shift at work. This shift pays 3x their regular rate – or about $1,000 (it’s a long shift!).

Your colleague says something along the lines of “no way I’m doing that, it’ll put me in a higher tax bracket and I’ll pay more in taxes!” He continues “I’m earning a $50,000 salary now in the 20% tax bracket, if I earn a dollar more, I’ll jump up to the 30% tax bracket and pay 10% more tax ($5,000 = $50,000 x 10% higher tax bracket) on everything. The government man, I tell you!”

Now, would it be a logical to structure the tax system with these “cliffs” where people are actually worse off if they earn more money? I hope you’ll agree that that approach wouldn’t make much sense.

Fortunately, the CRA (or “government man,” however you wish to colloquially refer to the tax collection division) agrees that this isn’t fair.

The CRA has designed the tax system to always encourage people to earn more money. The way they do this is that only the amount earned over $50,000 is taxed at 30%. The tax rate on anything less than $50,000 does not change…it says at 20%, regardless of how much income you earn!

If that colleague took the extra shift, his $50,000 salary will still be taxed at 20% and only the extra $1,000 pay (i.e. the amount over $50,000) will be taxed at 30%. So, he will still have $700 more in his pocket if he takes that shift ($1,000 pay less 30% tax on that). He still has to pay taxes on the extra money earned, but it’s still a pretty lucrative option for one [long] days’ work. I say he should do it!

Linking this back to Table 3, your colleague is thinking about option 1 (all income would be taxed at the higher rate). That’s the simple, tempting, but (fortunately for us) unfair and incorrect. Option 2 is how income tax is actually calculated.

Real Life Example

This is all great in theory, but doing this for all the 11 actual tax brackets is a pain in the arse. I agree – I just use an online calculator. For calculating taxes, I like to use this calculator from Ernst & Young. If you’re reading this some year later, substitute “2021” in the URL for the current year and you should get the current rates.

There are a bunch of columns of output, the important ones are:

Tax Payable

Marginal Tax Rate (this is the “tax bracket” corresponding to the income level from table 1 above, for Ontario)

Let’s take the calculator for a spin. Click on the link and first type in $60,000 into the “taxable income” box and press “calculate”. The result for Ontario is:

$10,622 tax payable (note this is a lot closer to Option 2 above than Option 1 from Table 3)

29.65% marginal tax rate (can you see that rate in table 1 above?)

This shows that if you’re in the 29.65% tax bracket, not all your income is taxed at 29.65%…otherwise you’d be paying $17,790 in tax ($60,000 x 29.65%). That’s a difference of over $7,000 compared to the actual $10,622 in tax you owe…amazing!

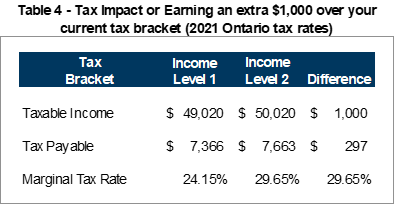

Another way to illustrate this is to compare incomes (using the EY tax calculator) that are just at and just above a tax bracket (similar to the extra shift conundrum your hypothetical colleague was discussing earlier):

This scenario is to highlight that earlier conversation with your colleague, but with real numbers. If you earn $1,000 over your current tax bracket, you pay, wait for it, only an extra $296.50 (it is not a coincidence that that equals the marginal tax rate for that higher bracket!).

What this means (for financial planning purposes) is that we can measure an incremental change to your taxes payable by only looking at your marginal tax rate (i.e. the rate for the tax bracket you’re currently in).

If you’re job hunting, taking an overtime shift, expecting a bonus, etc., use this calculator to see what the impact will be on your tax payable.

The Point

The main takeaway here is that earning more money can never result in less after tax income. The higher tax rate, if you “move up” a bracket, only applies to that extra income. All of your income below that bracket is taxed at the applicable lower rates.

Also, I’ve introduced the concept of a marginal tax rate (i.e. the current tax bracket you’re in) which is how we measure the tax impact from a change in your income. This is different (and more important) than your average tax rate, which we’ll dig into next.

Since there are a lot of acronyms and initialisms in personal finance (many of which are TLAs), I have included the following list to capture many of the ones that we will use here on LLB (aka LoonieLogic Blog):

ACB – Adjusted Cost Base

CAPE – Cyclically Adjusted Price-Earnings ratio

CDIC – Canadian Deposit Insurance Corporation

CCA – Capital Cost Allowance

CCP – Canadian Couch Potato

CPP – Canadian Pension Plan

CRA – Canada Revenue Agency

ETF – Exchange Traded Fund

FI – Financial Independence

FIRE – Financial Independence, Retire Early

GIC – Guaranteed Income Certificate

GIS – Guaranteed Income Supplement

LIRA – Locked-In Retirement Account

MER – Management Expense Ratio

OAS – Old Age Security

OSC – Ontario Securities Commission

RDSP – Registered Disability Savings Plan

RESP – Registered Education Savings Plan

RRIF – Registered Retirement Income Fund

RRSP – Registered Retirement Savings Plan

S&P500 – Standard & Poor’s index of the top 500 publically traded US companies

In the last post, we talked about the purpose of FI. You may have looked at the list of potential “whys of FI” and asked how that is different than normal retirement. Busted. It isn’t.

Remember just after I asked about what your goals are, I asked how fast do you want to get there? That’s the next big thing you need to decide.

I don’t care how old you are or what your time horizon is. You’re allowed to have the same goals. Maybe you’re just planning for it earlier or later than the next person. Traditional FI (aka regular retirement) is for those planning to be FI in their 60’s (maybe even 50’s). I would suggest that early FI would be for those targeting sometime in their 30’s or 40’s. This is what is referred to as FIRE (Financial Independence, Retire Early).

The key difference between traditional and early FI are societal norms. Society expects you to work until you’re in your 60’s (maybe 50’s if you’ve been prudent with saving or have an early pension option with your employer). Remember the commercials about “Freedom 55?” How many people laugh [hopelessly] when reminiscing about those ads? That’s because most people don’t retire that early.

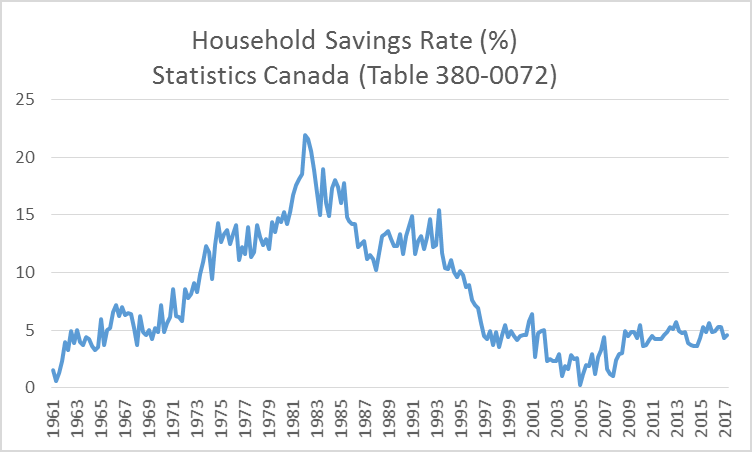

What drives the expectation of retiring in your 60’s? There are lots of reasons, but it comes down to your savings rate (what percent of your income do you save). The average Canadian household savings rate has been hovering around 5% for the last 20 years (See chart below). The 20 years before that was around 10-15%. Even in the 10-15% savings range, you are likely going to need 30-40 years to save enough for FI. Nothing wrong with that, you’re still better than average! However, most people I know do not like the idea of working full-time for 30 to 40 years and then benefiting from seniors’ discounts and driving your convertible to the lawn bowling tournament. This is not most people’s definition of happiness (but there’s nothing wrong if it is).

To target FI in your 30’s and 40’s will require a savings rate more like 40-60% (assuming you’re still in your 20’s or early 30’s). The math of this is relatively straightforward, but a topic for another day. Just trust me for now. The point is, if you want to get to FI earlier, you have to save more money. Ay Ay Captain Obvious!

Admittedly, this will be easier for those with high incomes, but there are also lots of examples of people on modest incomes achieving this.

If you’re saving around 50% of your income, you probably aren’t exhibiting all the regular behaviours of your peers. You didn’t lease a new car, you didn’t get the largest house the bank would let you, you don’t send your kids to private school (or an out-of-town university), you don’t go travelling around the world in fancy hotels, and so on. Most people would do all those things if they had the money. Early FI-ers have the money, but choose to save it rather than spend it on the same things as their peers.

The early FI group has the same goals as the traditional FI group, but they save a lot more of their income in order to get there faster.

The speed to which you want to reach FI is as important as the goal itself, as this will greatly affect how much you need to save each year. The more aggressive your goal, the more aggressive your savings plan has to be.

Conclusion

If you have an idea of what would make you happy, now you have to go the next step and decide when you want that to be. Once we have an idea of what and when, then we can start talking about how much money is needed.

Happy New Year! If you’re looking for a New Year’s resolution, then make it a goal to find your “Why of FI.” Remember that FI stands for Financial Independence.

One of the first questions I often hear people ask is “how much do I have to save to retire?” That’s like jumping in my car (yes, I own a car in case you’re judging) and asking how long the drive is going to be without having any other details. If I said it’ll take 20 hours, you might just get out of the car and ignore anything else I had to say. That’s what would happen if I said you needed $x hundreds of thousands or $x millions to be FI.

There are many questions that need to be answered before determining the length of the trip. The most important is where you want to go. Then we can talk about the mechanics – how fast is the car, can you buy enough gas to get there, what are the speed limits, where do you want to stop along the way, dangers to avoid, etc.

The same questions apply to FI – where do you want to go? What are your goals? How fast do you want to get there? What is the limit of your income? What are the risks to your finances? Most of these I cannot answer for you and I still sometimes struggle with myself.

What is your why of FI?

Your why is going to make the journey much easier. It will provide purpose and motivation on days when you feel like giving up. There isn’t much purpose to FI if you don’t have a why. It is easy to skip this and go straight into the math, but don’t bother scrolling down…there will be no math today.

The ChooseFI podcast, which does a good job of curating guests and topics from the FIRE community (Financial Independence & Retire Early). They have a great episode about the Why of FI. Just a note that this episode does reference the retiring early (“RE”) part. I try not to focus on the “RE” part of FIRE, you are free to work as much or as little as you want after you reach FI. Whether or not you retire early, the reasons are very similar.

Some common whys:

Pursue your hobbies

Making art, furniture, etc.

Travelling

Reading / Writing

Hiking / Jogging / Swimming / Golfing

Gardening

Cooking

Camping / RVing

Etc.

Spend time raising your children or grandchildren

Taking care of ageing parents

Start a business you’ve dreamed about

Change careers

Volunteer

Live somewhere else

Keep healthy (avoid workplace emotional or physical stress)

Mitigate job loss risk (ageism and technological obsolesce)

Etc.

Notice that some of those still involves working and/or making money? Just because you’re FI doesn’t mean you’re forever barred from making money. The point is you don’t have to make money. You can if you want to, but you don’t need to.

I’m still working on my “why” but I like the idea of spending more time talking to people about finances and working on people’s financial plans (whether or not they can afford to pay me). Also, moving to a smaller community and getting involved is also an intriguing idea. I’ll likely still stay engaged in my current career, but may scale that back a bit to make room for other things.

At this point, you might not have any idea. You might be like an eight year-old wanting to be an astronaut when they grow up. What makes sense, what is realistic? Liz over at Frugalwoods had a great post about how to figure out what to do with your life. This would be a great first step towards figuring out your why of FI.

Even the idea of early retirement may strike a chord with you. However, you have to think about why that is. Is it because you loathe your job and can’t wait until you flip off your boss, sleep in and Netflix all day? That thrill will only last a few months until you start to get bored. There has to be some overarching plan of what you’ll do with the extra 10+ hours per day.

Happiness

Many of your goals will likely come down to happiness. The Happy Philosopher talks about this in the context of alligators and kittens. That is, alligators make you unhappy, kittens make you happy.

Assuming you have both alligators and kittens in your house, you have two options:

Remove the alligators

Add more kittens

Suppose it to say, that if there are any alligators in your house, adding more kittens will not make you much happier. You need to remove the alligators first. Then, you will get much more happiness from your existing and future kittens.

Frederick Herzberg, is an American psychologist best known for his motivator-hygiene theory. This theory has been in business school textbooks for decades. The idea is that there are both satisfiers (kittens) and dissatisfiers (alligators) in your life (or job), which act independently. For example, if you remove an alligator, you will not automatically become happy. However, having an alligator in the house can prevent you from being happy, even if you have lots of kittens.

Say you have a horrible boss, so much so that you think, “if only my boss wasn’t such an asshat, then I would be happy.” If you did get a good boss, you’re not automatically going to be happy. You still need satisfiers/kittens to be happy (such as interesting work, engaging colleagues, proper compensation/recognition, etc.). However, having that asshat boss can certainly prevent you from being happy.

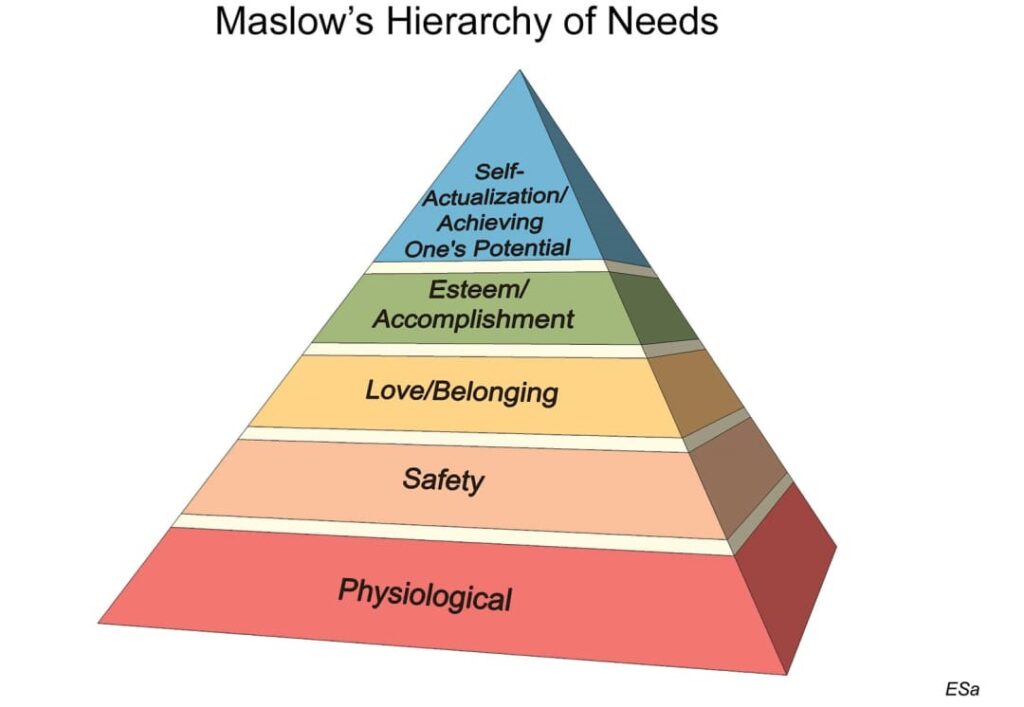

Another, even more common business theory is Abraham Maslow’s hierarchy of needs, which is depicted by the following pyramid. This is equally important in your personal life.

Image Credit: J. Todd Robinson, AIA, ESA (as it appears on asa.org)

The goal is to reach the top of the pyramid. Self-actualization or “achieving one’s potential” is the definition of success and happiness. However, you cannot achieve that if you don’t already have the building blocks below it.

For example, it would be hard to achieve a feeling of safety if your physiological needs (food, water, shelter) are not met. It would be hard to feel loved or have a sense of belonging if you fear for your physical or financial safety.

Money can help you reach the top of the pyramid, but truthfully, its biggest contribution is to the first two layers, physiological and safety. You’ll need to look elsewhere to get to the top.

Take the time to assess your life and determine what building blocks you need, or what dissatisfiers/alligators you need to get rid of. Only then, can you move towards happiness.

Conclusion

If you can figure out what makes you happy, then you’ve probably figured out your “why of FI.”

The goal of FI is to be happy. Money cannot make you happy by itself, but it is a tool to let you pursue the things that will make you happy. Only you can decide what those things to pursue are. I can’t tell you how much money you need to be FI until you can describe to me the life you want to live after you’ve reached it.

I do get a kick out of excessive quotation marks (on paper or the “air” variety). A “road map” (and I’m doing air quotes here) is appropriate because it probably won’t be followed and is just some hypothetical construction to make us all feel better because there is a “plan” in place. But just because nothing ever goes to plan doesn’t mean having a plan is not important.

The plan here is to cover four key categories that are particularly pertinent to FI, which are listed below. They are all interrelated to some extent, but really start with saving some money (or paying down debt).

This gives you an idea of the types of topics that we’ll delve into and maybe, if I figure it out how to, I’ll link the following list to the tags for the articles.

Debt and Savings

Psychology

Income

Analyses / Strategies

Investing

Investments

Asset Allocation

Tax Advantaged Accounts (RRSP, TFSA, RESP, etc.)

Living

Insurance

Hobbies

Health

FI (Financial Independence)

Goals

Target Amount Required

Withdraws and Taxes

Debt and Saving

Debt and saving are polar opposites. This category is for getting started and continued tweaking throughout your life.

It covers how to get out of debt in the first place so that you can start saving money.

It covers how you go about tracking your finances. How do you create a gap between your income and your expenses so that there is money available to save? Can you increase your income? Which expenses can you decrease?

Investing

This category focuses on where to put the dollars you have saved.

Ideas of what to invest in, appropriate asset allocations, which types of accounts to use, robo-advisors, stocks, bonds, mutual funds, ETFs, and the like.

It also dives into the cost of investing in various different ways.

Living

Once the saving and investing is humming along, you still have to enjoy your life…being happy and healthy! This includes looking into hobbies (which may help you figure out your why of FI – more on that later!) and risk management strategies / insurance to avoid things that will derail your finances in a heartbeat.

Financial Independence

This category includes how much money you actually need to fulfill your goals (and how you might figure out those goals in the first place).

Once you’ve reached FI, the work doesn’t stop…there are still a lot of moving pieces to manage and maximize the money you have saved. This includes tax minimization, risk minimization, sequence of return considerations, withdrawal plan (which account and when), etc.

I hope that gives you a more in-depth overview of the topics you will find here on Loonie Logic. If you have specific suggestions for other roads to travel, by all means, let me know!

Happy Canada Day! This blog is about Canadians and their money and the how, why and where you should save, protect and invest yours!

I hope this blog will resonate with new and experienced Canadians alike.

I would be remiss not to mention the COVID-19 pandemic. We are starting to economically recover from it, however, that will likely be a multi-year process. The aim is that this blog will assist, motivate and encourage anyone at any stage (pandemic or not!) to prioritize your finances and line you up for success.

Money migrating meticulously

Loons are amazing birds. They can be spotted across North America and occasionally in further-flung places such as Iceland. In the summer, many of them hang out on our lakes in Canada. When I think of loons, I think about canoeing across a northern Ontario lake. Thoughts of peace and tranquility ensue.

At the risk of a bad segue, the loon is also a symbol of the Canadian dollar: our dollar coin, known as the “Loonie.” Our dollars should likewise bring feelings of peace and tranquility. Wait…did I just hear a quiet “Ha! Yeah right” mumbled under your breath? Was my analogy too cheesy? Too bad…let’s continue.

Loons have a purpose – they have goals. They often travel thousands of kilometres in order to survive and thrive. Flying south to find non-frozen bodies of water, traversing clear lakes and diving for several minutes to catch a fish.

How do they know they are going in the right direction?

How do you know if you are going in the right direction?

#AnalogyOver

I’ll propose that we’re all going in the same direction, and it’s called financial independence (“FI”). FI has a multitude of meanings to different people. A simple definition of FI is that you have enough money such that working for more money is optional. This can be as simple as traditional retirement around age 65 give or take, but it can also encompass other goals.

The “FI community” generally advocates frugality and saving a high percentage of your income with the goal of attaining FI earlier than the average age-65 retirement. Some choose to achieve FI with a goal to retire early (“RE”). Combining RE with FI is referred to as “FIRE”.

If you want to learn more about FIRE, I suggest you watch the new documentary (or the book by the same title) that came out last year called “Playing with FIRE.” Loonie Logic is a proud supporter of this project and helped it get off the ground with its Kickstarter campaign. Look closely in the credits of the film for yours truly!

While I do like to find a good deal and to optimize my spending, I would not call myself frugal and I don’t fit perfectly into the FIRE mentality. Savings strategies have an important role to get to FI, but I won’t give you a hard time about what you purchase (unless it was at regular price, lol). I have a bit of the FIRE mentality in me, but that’s not the main thing I want to focus on.

For me, FI is about having a choice. I view money as a tool to achieve your goals. If you have enough money, then it gives you the freedom to choose what to do with your time. You will not be obligated to trade your time for money (aka working[1]), although, no one is going to stop you if you enjoy it or have a good use for more money. Other things you could choose to do with your time include travelling, spending time with your kids, pursuing a hobby, volunteering, changing careers, or just slowing down your life so that you can stop and smell the proverbial flowers.

Credit to the talented Bill Waterson

This is not dependent on age, but rather defined by a mentality. A mentality of intentional living, ignoring societal norms, focusing on fulfilling your life rather than have it filled with others’ goals and expectations.

Expect to see posts about once a month, with the occasional interjection as events unfold and thoughts arise. Next month, you’ll see a road-map of where this blog is likely to go and a better idea of the types of topics to look forward to.

As a flock, we can migrate our money into more prosperous territory and be farther ahead than a lone wolf on Wall Street.

[1] Shout out to Vicki Robins for the trading “life energy” for money concept